Regulated vs Offshore Forex Brokers: An Honest Risk Assessment

This article is for informational purposes only and does not constitute financial or legal advice. Always conduct your own due diligence before depositing funds with any broker.

Choosing between a regulated and an offshore forex broker is one of the most consequential decisions you’ll make as a trader, and most traders make it without fully understanding what they’re actually choosing between. This article gives you a structured, honest framework for assessing broker safety across both categories, so your decision is based on how regulation actually works.

The regulated vs offshore forex brokers debate is rarely black and white. Regulation varies wildly in quality and enforcement. What matters is understanding the specific protections and gaps that apply to your situation.

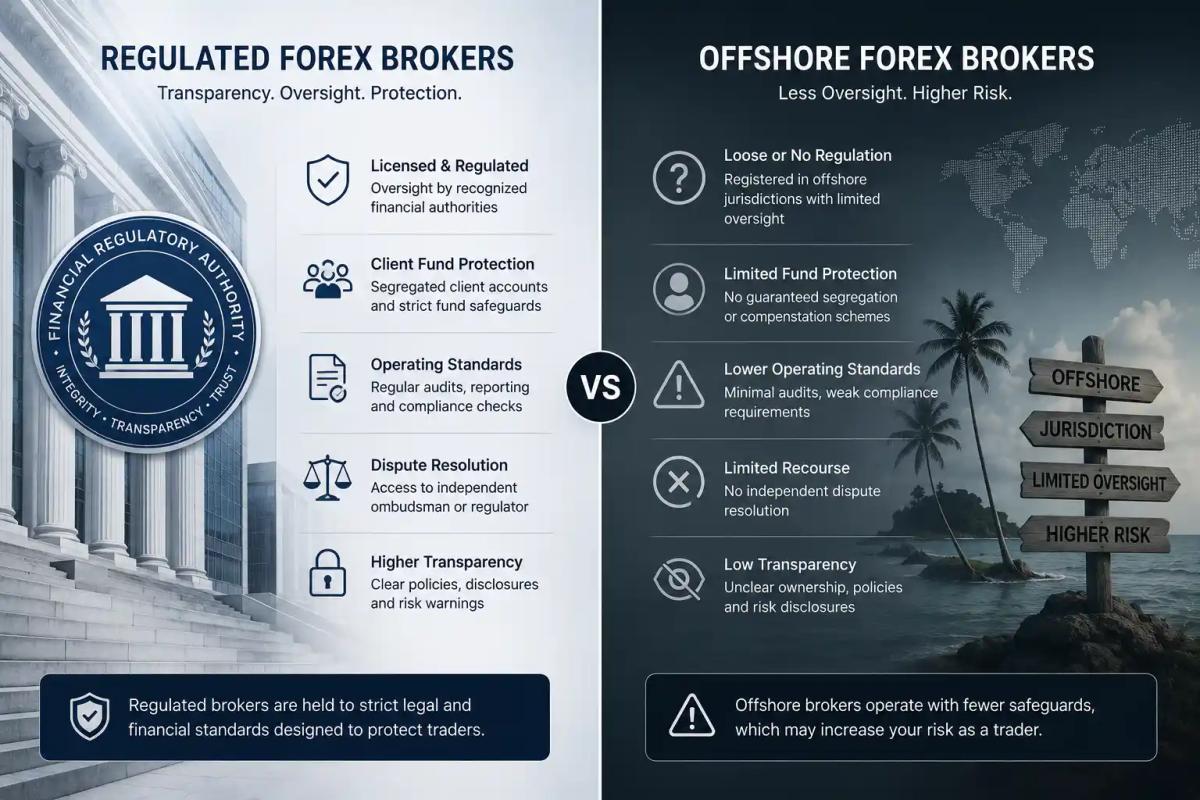

What Broker Regulation Actually Does (and Does Not) Protect You From

Regulation sounds reassuring until you ask what it actually does on a bad day. Really, it depends entirely on which regulator issued the license, what legal obligations come with it, and whether those obligations are actively enforced.

Broker regulation is a framework for operational conduct. It sets rules around how a broker handles your money, how it executes your trades, and what happens if the firm runs into financial trouble.

Capital Segregation and Investor Compensation Schemes

The most important protection regulation can offer is client fund segregation. Under this requirement, your money must be held in accounts separate from the broker’s operational funds. If the broker goes insolvent, creditors cannot simply sweep your trading balance into the general pile.

When a regulated broker collapses, segregated client funds are typically returned in full or substantially recovered. Without segregation, your deposit is effectively an unsecured loan to the broker, and you join the queue with every other creditor.

Beyond segregation, some jurisdictions operate investor compensation schemes. The UK’s Financial Services Compensation Scheme (FSCS) covers eligible clients up to £85,000 if a regulated firm fails. Cyprus’s Investor Compensation Fund (ICF) covers up to €20,000. These provide a defined floor when things go badly wrong.

Compensation schemes cover firm failure, not trading losses. If you make poor trades and lose your capital, no scheme covers that. These protections exist for the scenario where the broker is the problem, not your strategy.

Regulatory Jurisdiction and Enforcement Reach

A regulator is only as effective as its enforcement reach. The FCA can fine, suspend, or shut down a UK-authorised firm. It can pursue legal action through UK courts and compel brokers to return client funds.

An offshore regulator operating in a small jurisdiction has far less practical power to compel anything. Even if it technically rules in your favour during a dispute, enforcing that ruling against a broker operating across multiple jurisdictions is a separate problem entirely.

This is the enforcement gap. The ability to act on them quickly and meaningfully varies enormously across regulatory environments.

That enforcement gap becomes clearer once you understand what the tier system actually means for your money.

The Regulatory Tier System: Not All Licenses Are Equal

If you’ve seen brokers displaying logos from multiple regulators, you already know the landscape is crowded. What you need is a way to rank those licenses by what they actually mean for your money.

Tier 1 Regulators (FCA, ASIC, CySEC, NFA/CFTC)

Tier 1 regulators are the benchmark. They share common characteristics: robust rulebooks, active enforcement divisions, capital adequacy requirements, mandatory client fund segregation, and in most cases, compensation schemes or negative balance protection requirements.

The key Tier 1 bodies and what they govern:

- FCA (Financial Conduct Authority) – United Kingdom. Requires segregated accounts, negative balance protection for retail clients, FSCS compensation up to £85,000 , and strict leverage caps under ESMA-influenced rules.

- ASIC (Australian Securities and Investments Commission) – Australia. Strong segregation requirements, leverage caps introduced in 2021, active enforcement track record.

- CySEC (Cyprus Securities and Exchange Commission) – Cyprus/EU. Operates under MiFID II framework, ICF compensation scheme, passporting rights across the EU. Has faced criticism for inconsistent enforcement historically, but remains a credible Tier 1 body under EU regulatory architecture.

- NFA/CFTC (National Futures Association/Commodity Futures Trading Commission) – United States. Extremely strict by global standards. FIFO rules, no hedging, tight leverage caps (50:1 on major pairs), and one of the most demanding compliance environments in the world.

Tier 2 and Tier 3 Regulators: The Grey Zone

Tier 2 regulators operate in jurisdictions with genuine regulatory intent but more limited enforcement infrastructure or narrower scope. South Africa’s FSCA (Financial Sector Conduct Authority) is a reasonable example: it has real requirements, but its legal reach and compensation mechanisms don’t match the Tier 1 standard.

Tier 3 is where things get genuinely murky. These are regulators with low capital requirements, minimal enforcement activity, and licenses that are obtainable with relative ease. They provide a veneer of regulatory status without the substance. Some brokers hold Tier 3 licenses alongside Tier 1 authorisations, routing certain client segments through the weaker entity.

Offshore Jurisdictions Commonly Used by Forex Brokers

Several jurisdictions appear repeatedly in the broker space precisely because their licensing requirements are lighter and oversight is limited:

- Seychelles – Regulated by the FSA (Financial Services Authority, Seychelles). Low capital requirements, minimal active enforcement. Popular for brokers offering higher leverage to non-EU, non-UK clients.

- Vanuatu – Regulated by the VFSC (Vanuatu Financial Services Commission). Very accessible licensing, limited regulatory resources.

- Saint Vincent and the Grenadines (SVG) – SVG does not regulate forex brokers at all. The registered companies you see based there are simply incorporated. The SVG FSA has repeatedly stated it does not supervise forex trading activity.

- Belize – Regulated by the IFSC (International Financial Services Commission). Has a regulatory framework on paper but is widely considered a Tier 3 environment.

Understanding which jurisdiction your broker is actually operating under is step one in any honest safety assessment.

The Real Risks of Trading with an Offshore Broker

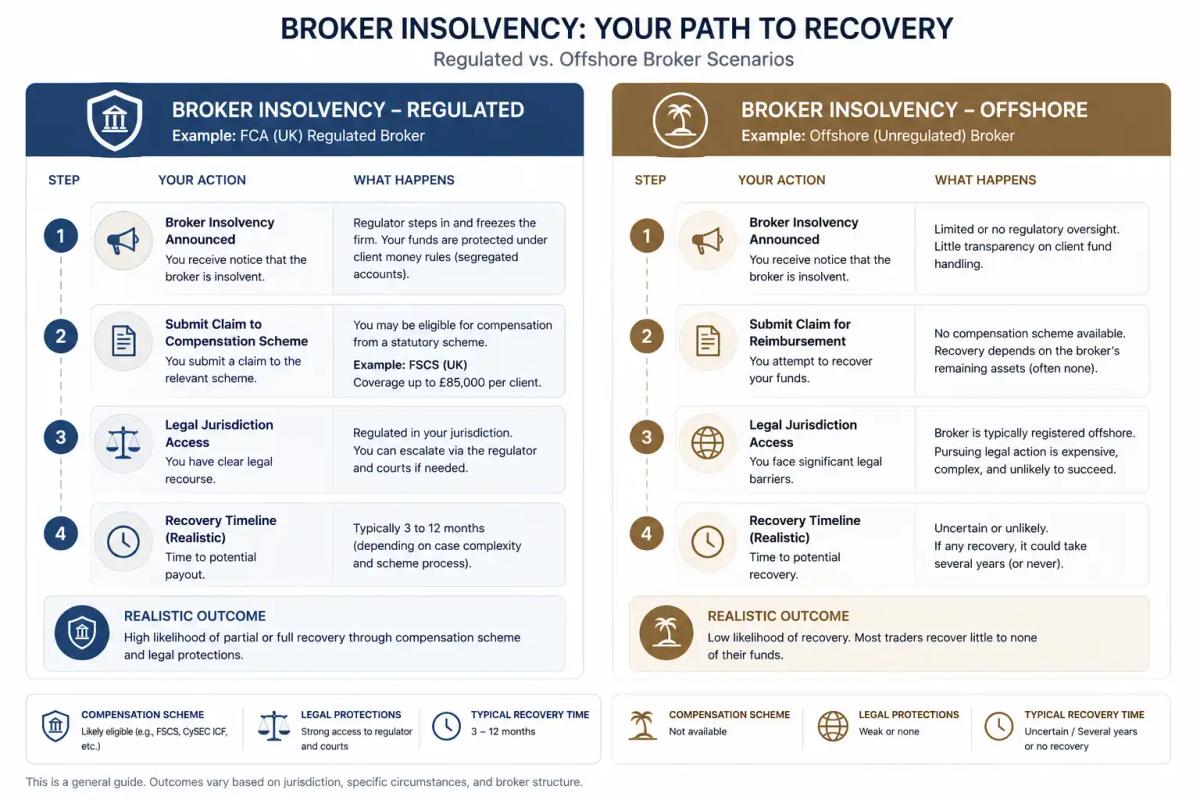

Fund Recovery in a Dispute: What Your Options Actually Are

Suppose your offshore broker freezes your account, delays withdrawals indefinitely, or simply goes quiet. Your practical options at that point are limited.

You can file a complaint with the offshore regulator, which may or may not respond, and almost certainly cannot compel the broker to act quickly. You can pursue civil litigation in the broker’s home jurisdiction, which involves navigating a foreign legal system, probable language barriers, and costs that often exceed the value of the dispute. There is no compensation scheme to fall back on, and no guaranteed timeline for resolution.

With a Tier 1 regulated broker, the process is different. You have:

- A defined complaints procedure

- A regulatory escalation route through the FCA or equivalent

- Access to an ombudsman or arbitration service

- A compensation scheme with a defined payout ceiling in a worst-case insolvency scenario

None of this is instant, and none of it guarantees a full recovery. But the infrastructure exists and it has legal teeth.

The probability of meaningful fund recovery after an offshore broker dispute is lower than with a Tier 1 entity. That’s a statement about the structural reality of enforcement, not a categorical judgement about intent.

Leverage, Restrictions, and Why Offshore Brokers Offer Them

Offshore brokers routinely advertise leverage ratios of 200:1, 500:1, or higher. That isn’t a customer service decision. It’s a consequence of operating outside the leverage caps imposed by Tier 1 regulators.

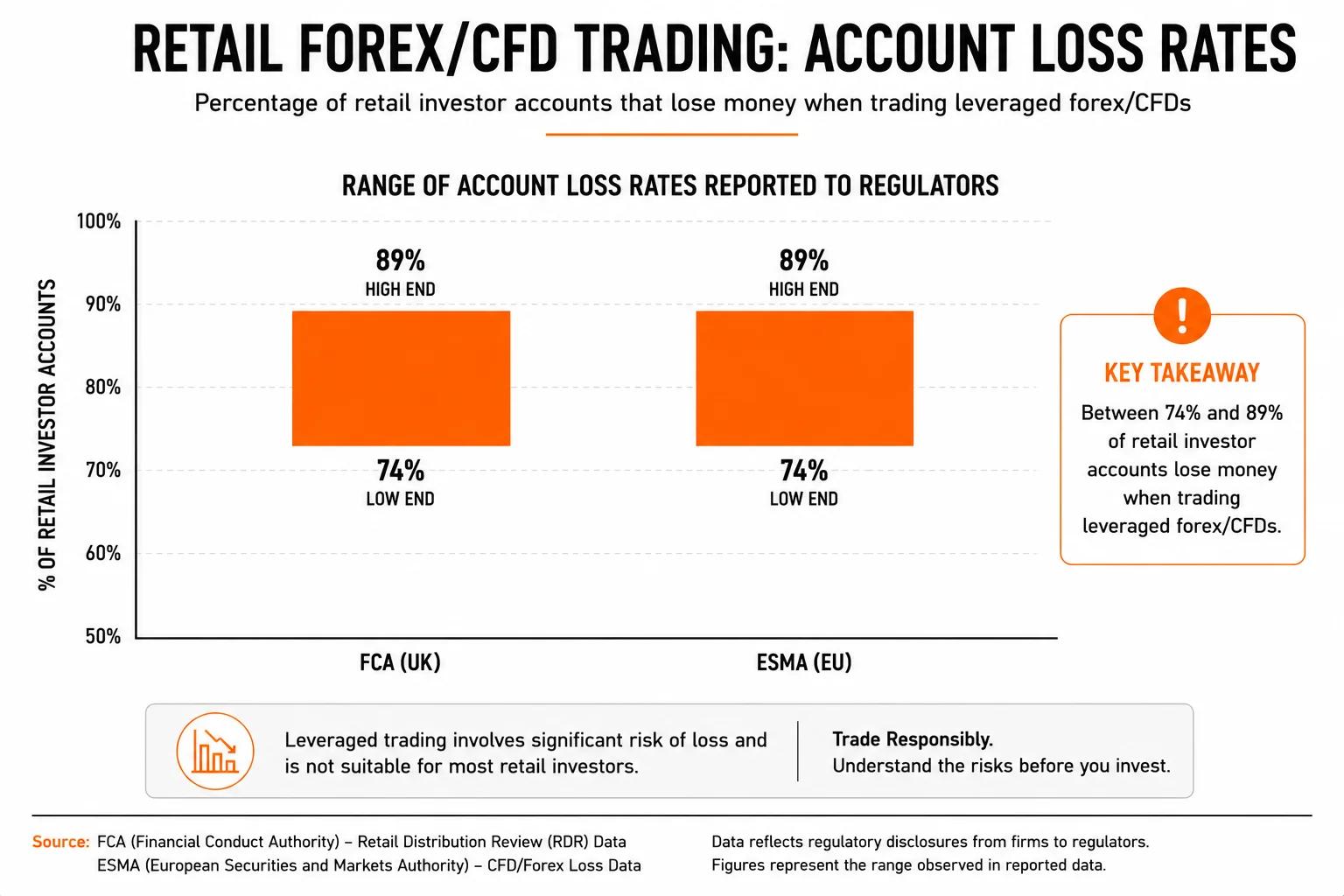

The FCA and ASIC cap retail leverage at 30:1 on major forex pairs. Those caps exist because higher leverage dramatically increases the speed at which a losing position can exceed the account balance. Regulators saw enough retail accounts wiped out to mandate the restriction.

Offshore brokers face no such requirement. That’s useful for traders who understand and actively manage leverage risk and dangerous for traders who don’t.

Operational and Counterparty Risk

When you trade with a forex broker, especially one operating on a dealing desk model, you are in some cases trading against the broker itself, meaning it takes the other side of your position.

An offshore broker with thin capital reserves and no mandatory capital adequacy requirements carries real counterparty risk: if enough clients are profitable simultaneously, or if the broker is poorly capitalised, it may not be able to meet its obligations.

So why do experienced traders sometimes choose this environment deliberately?

Why Some Traders Deliberately Choose Offshore Brokers

Regulated brokers aren’t universally preferred, and it’s worth being honest about why. Some traders make an informed choice to trade offshore, and understanding their reasoning tells you something useful about the tradeoffs involved.

Instrument Access and Leverage Caps

Tier 1 regulation restricts what retail traders can access and at what leverage. If you want 100:1 leverage on exotic currency pairs, you won’t find it under FCA or ASIC authorisation as a retail client. Offshore brokers offer significantly wider instrument access and leverage ratios unavailable in regulated environments.

For traders with substantial experience who actively use leverage as part of a deliberate strategy, the restriction is a genuine operational constraint, not just an inconvenience. Understanding how good broker risk management practices interact with leverage access is worth exploring before you make that call.

Account Types, Deposit Minimums, and Cost Structure

Offshore brokers often compete on cost and accessibility. Lower minimum deposits, raw spread accounts with lower commissions, and account structures that wouldn’t survive the compliance overhead of a Tier 1 environment are common draws.

Some traders are looking for specific execution conditions and are willing to accept higher risk in exchange for better cost structure. That’s a rational calculation, provided it’s made with full awareness of what’s being traded off.

Restrictions Imposed by Top-Tier Regulation

Beyond leverage, Tier 1 regulation introduces a range of restrictions that some traders find operationally limiting:

- Negative balance protection is mandatory (which benefits most traders, but removes a tool in edge-case hedging strategies)

- Margin close-out rules require positions to be liquidated at a specified threshold

- Marketing restrictions on certain account types or bonus structures

- Some instruments are unavailable to retail-classified clients without professional reclassification

Professional client classification exists as a route to fewer restrictions under Tier 1 regulators, but it requires meeting specific capital, experience, and trade frequency thresholds. Not every trader qualifies.

How to Assess a Broker’s Safety: A Practical Checklist

Theory gives you a framework. A process you can actually run gives you an answer.

Verifying Regulatory Status (and Spotting Clone Firms)

Clone firm fraud deserves direct attention. Clone firms impersonate legitimate regulated brokers, using their names, license numbers, and branding to appear credible. You find what looks like a well-known regulated broker, but the website you’re on belongs to a completely separate and fraudulent entity.

To verify a broker’s actual regulatory status:

- Go directly to the regulator’s official website, not the broker’s website.

- Use the regulator’s authorised firm register to search by the broker’s exact legal entity name.

- Cross-check the license number and the contact details listed on the register against what the broker’s site shows.

- If anything doesn’t match (including the legal name, address, or license number) treat it as a red flag and stop.

The FCA’s register is at register.fca.org.uk. ASIC’s is at search.asic.gov.au. CySEC’s is at cysec.gov.cy. Use them.

Fund Protection Mechanisms to Look For

When evaluating a broker’s fund protection structure, check for:

- Explicit confirmation that client funds are held in segregated accounts at named third-party banks

- Membership in a named compensation scheme (FSCS, ICF, or equivalent)

- Audited financial statements or references to independent auditing

- Negative balance protection for retail accounts

- Clear documentation of what happens to your funds in an insolvency scenario

A broker that can’t or won’t answer direct questions about fund segregation has already told you something useful.

Red Flags That Indicate Elevated Risk

Regardless of jurisdiction, the following patterns indicate elevated risk:

- Withdrawal delays or complaints about withdrawal denials (check independent forums and review aggregators)

- Guaranteed return claims or unrealistic performance projections

- Pressure to deposit additional funds before a withdrawal is processed

- Regulatory credentials that don’t match the register when verified directly

- No physical address or verifiable corporate structure

- Bonuses structured in ways that tie up withdrawals (common in lower-tier environments)

None of these are exclusive to offshore brokers. They appear occasionally in regulated environments too. The difference is that under Tier 1 regulation, you have formal escalation routes when they do. Our forex broker comparison guide covers how these factors play out across specific brokers if you want to go deeper.

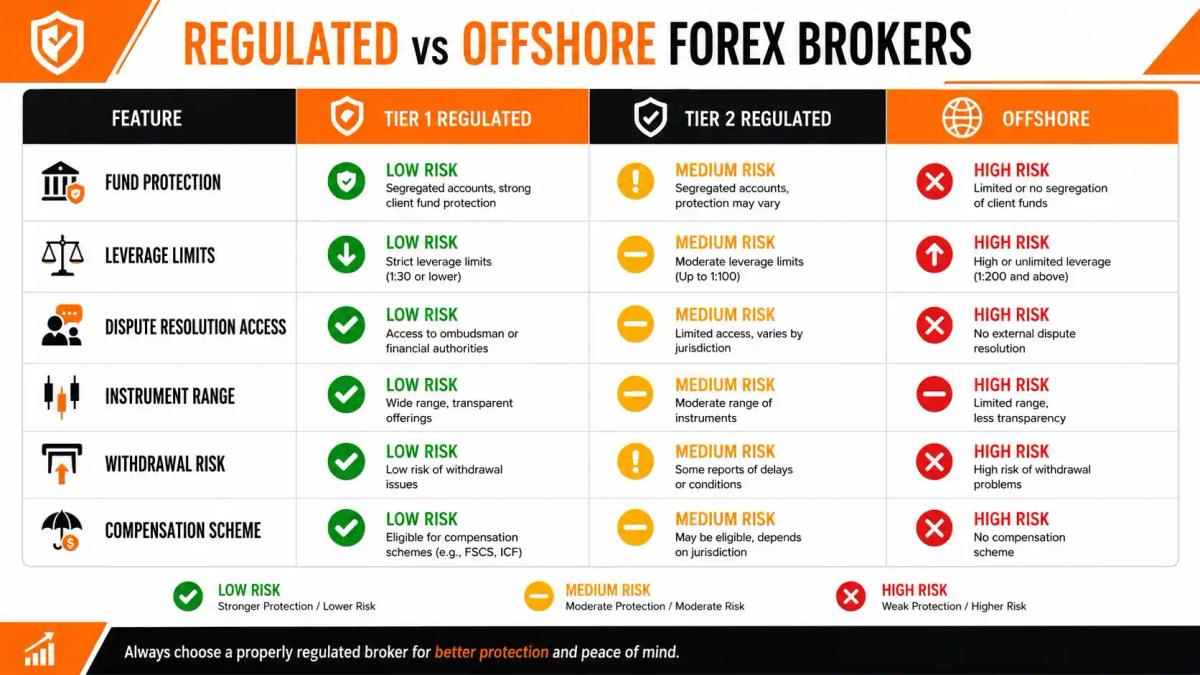

Regulated vs Offshore Brokers: Side-by-Side Comparison

The protections and restrictions covered above stack up very differently depending on which type of broker you’re with. This table maps the key variables side by side, so you can see exactly where the gaps are before you commit funds.

Which Type of Broker Is Right for Your Situation?

Your answer depends on what you’re prioritising and how clearly you understand the tradeoffs.

A Tier 1 regulated broker is the appropriate default for most retail traders. The fund protections are real, the dispute resolution infrastructure exists, and the restrictions (including leverage caps, negative balance protection, and margin close-out rules) are largely designed to prevent the kind of catastrophic losses that end trading careers early. For anyone building a long-term trading operation where capital preservation matters, this is the rational baseline.

An offshore broker becomes a considered choice rather than a default when you have specific, well-defined operational needs that Tier 1 regulation restricts:

- You require leverage ratios beyond the retail cap for a defined strategy

- You want access to instruments not available under your current retail classification

- You’re funding at a scale where you’ve assessed and accepted the risk/reward of the offshore environment

That calculation carries real, elevated risk, and that risk should be priced into the decision explicitly rather than glossed over because the broker’s marketing is persuasive.

Regardless of which direction you go, apply these principles:

- Verify the license directly through the regulator’s register. Every time.

- Use only funds you can afford to lose entirely if the broker fails.

- Understand the fund recovery process before you need it, not after.

- Read the withdrawal terms before depositing, not the day you want to withdraw.

Your job is to understand exactly what risk you’re carrying and decide whether that’s acceptable for your situation.

Frequently Asked Questions

What does the regulatory tier system actually mean for my money as a retail trader?

The tier system reflects how much legal protection, enforcement infrastructure, and fund recovery mechanism backs your account. A Tier 1 broker (FCA, ASIC, CySEC) means segregated funds, potential compensation scheme coverage if the firm fails, and a regulatory body with real enforcement power. A Tier 3 or offshore license means you may have few or none of those protections in practice, even if the broker claims to be regulated.

Can an offshore broker ever be a reasonable choice?

Yes, in specific circumstances and with a clear understanding of the risks involved. Some experienced traders use offshore brokers for leverage access, instrument range, or cost structures unavailable under Tier 1 regulation. The key distinction is informed choice: you understand that dispute resolution options are limited, fund recovery is less certain, and counterparty risk is higher before committing capital.

If an offshore broker refuses my withdrawal, what can I actually do?

Your realistic options are limited. You can file a complaint with the offshore regulator, though enforcement outcomes are uncertain and typically slow. You can attempt civil litigation in the broker's home jurisdiction, which is costly and logistically difficult from abroad. Some traders have had success disputing charges through credit card providers if the initial deposit was made by card, but this depends on the circumstances and your card issuer's policies. There is no ombudsman, no compensation scheme, and no fast regulatory escalation route available in the way that exists under Tier 1 regulation.

How do I confirm that a broker's regulation is genuine and not a clone firm?

Go directly to the official regulator's website and search the authorised firm register using the broker's legal entity name. Cross-check the license number, registered address, and contact details shown on the register against what appears on the broker's website. If there's any discrepancy, particularly in the legal name or license number, do not deposit funds. The FCA register (register.fca.org.uk), ASIC register (search.asic.gov.au), and CySEC register (cysec.gov.cy) are publicly accessible and free to use.

Does the FSCS cover all my losses with a regulated broker?

No. The FSCS covers eligible clients up to £85,000 specifically in the event of a regulated firm's failure — meaning the broker itself becomes insolvent and cannot return client money. It does not cover trading losses, poor investment decisions, or disputes about execution. The compensation scheme is a last-resort mechanism for firm failure, not a general insurance policy on your trading account.

What is negative balance protection and which brokers are required to offer it?

Negative balance protection means your account cannot fall below zero. If your losses exceed your account balance, the broker absorbs the difference rather than pursuing you for the deficit. Tier 1 regulators including the FCA and ASIC require this for retail clients. Offshore brokers are not required to offer it, though some do. If you're trading with high leverage and an offshore broker without negative balance protection, a fast-moving market can, in principle, leave you owing money beyond your initial deposit.

How do leverage restrictions under Tier 1 regulation compare to what offshore brokers offer?

Under FCA and ASIC rules, retail clients are capped at 30:1 leverage on major forex pairs , with lower limits on minor pairs and other instruments. Offshore brokers routinely offer 200:1, 500:1, or higher with no regulatory ceiling. Higher leverage amplifies both gains and losses: a 0.2% adverse move at 500:1 wipes the account. The caps imposed by Tier 1 regulators exist because the data on retail trading outcomes made the risk clear enough to mandate a ceiling. Type your paragraph here

About the authors

Related articles

How Much Do Forex Traders Actually Make? A Realistic Income Breakdown

A realistic, data-grounded breakdown of forex trader income across four trader types, from part-time retail to institutional, including what account size actually means for your earnings.

Which Forex Brokers Have the Most Complaints? What Regulatory Records Actually Show

Learn how to check forex broker complaint records across FCA, ASIC, NFA, and CySEC databases; and what those records actually tell you before you open an account.

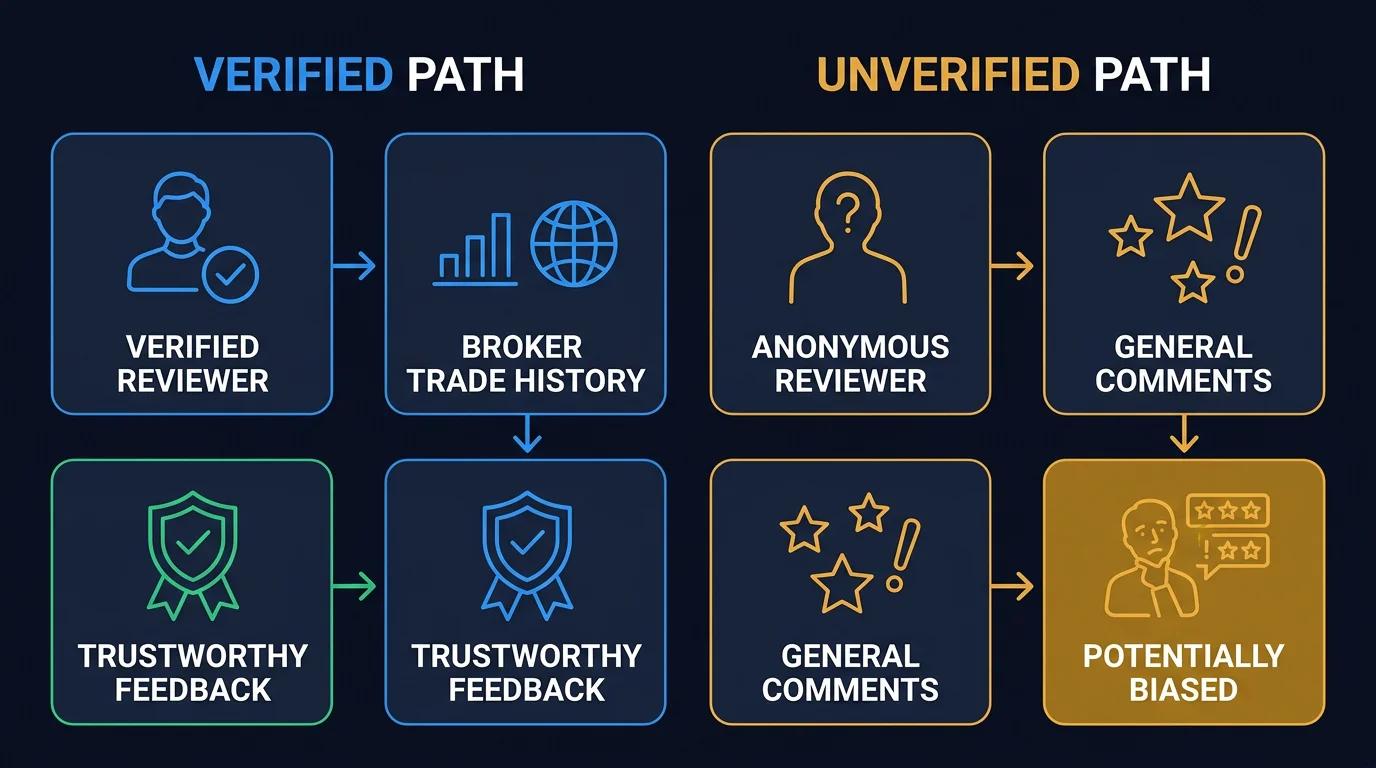

Verified vs Unverified Forex Broker Reviews: What the Difference Actually Means

What "verified" actually means on broker review platforms, how to spot fake review campaigns, and how to build a credibility framework that surfaces genuine signal before you open an account.

0 comments