What Are Derivatives? A Beginner’s Guide to Derivative Instruments

Derivatives trading accounts for one of the largest and most active segments of global financial markets. For newcomers, the term can feel abstract or unnecessarily complex. The core concept is actually straightforward once the basic mechanics click into place.

This guide covers what derivatives are, how they work, and the role they play in modern finance. By the end, you should have a working foundation for understanding these instruments and enough to explore specific derivative types with confidence.

What Is a Derivative?

A derivative is a financial contract whose value depends on something else. That “something else” is the underlying asset, and it can be almost anything with a measurable price: stocks, bonds, commodities like oil or wheat, currencies, interest rates, or broad market indexes.

The derivative itself is not the asset. It’s an agreement between two parties that references the asset’s price. When that price moves, so does the value of the contract.

How Derivatives Derive Their Value

The link between a derivative and its underlying asset is what makes the contract worth anything at all. A simple example: suppose you hold a contract giving you the right to buy gold at a fixed price. If gold’s market price climbs, your contract gains value: it now lets you purchase gold below what everyone else is paying.

Inversely, if the underlying asset moves against your position, the derivative loses value. In effect, the contract tracks or responds to price movements in the underlying market, though the precise relationship varies by contract type.

Why Do Derivatives Exist?

Derivatives exist because they solve real problems in financial markets. Understanding these purposes makes the instruments themselves easier to grasp.

Hedging Risk

Risk management drives much of derivatives activity. Businesses and investors use these contracts to shield themselves from unfavorable price swings.

A farmer worried about crop prices dropping before harvest might lock in a selling price today through a derivative contract. An airline facing unpredictable fuel costs might secure more stable expenses the same way. This process (reducing exposure to price fluctuations) is what we call hedging.

Speculation

Protection isn’t the only motive. Some traders use derivatives to profit from expected price movements without ever owning the underlying asset. This is speculation.

Since derivatives often require less capital upfront than buying the asset outright, they can appeal to traders with a directional view on prices. That same characteristic, however, means potential losses are amplified too.

Price Discovery and Market Efficiency

Derivatives markets also contribute to the broader financial system by helping establish prices. When large numbers of participants trade based on their expectations for future prices, the collective activity generates useful information about where markets believe prices are heading.

This price discovery function helps incorporate diverse views and information into asset valuations.

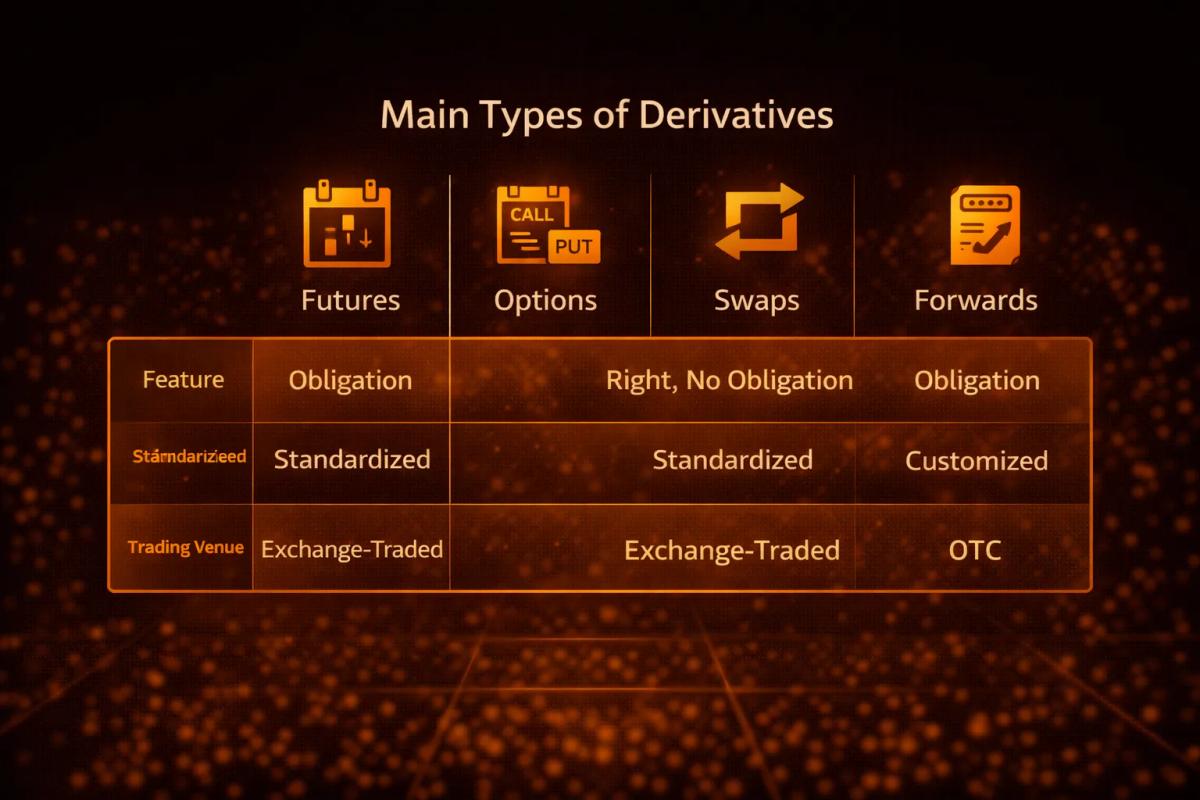

Main Types of Derivatives

Four categories account for most derivatives activity. Each has characteristics that suit different purposes.

Futures Contracts

A futures contract commits both parties to buy or sell an asset at a set price on a specific future date. Both sides must fulfill the contract at expiration, there’s no opting out. Futures are standardized: contract size, expiration dates, and other terms are fixed by the exchange where they trade.

Futures cover commodities like oil, natural gas, and agricultural products, along with financial instruments such as stock indexes and currencies. Standardization and exchange trading make these contracts relatively liquid and transparent.

Options Contracts

An options contract grants the buyer the right (but not the obligation) to buy or sell an underlying asset at a specified price before or on a certain date. The seller, by contrast, must fulfill the contract if the buyer exercises that right.

Two basic types exist: call options (the right to buy) and put options (the right to sell). Because options offer flexibility without requiring action, buyers pay a premium upfront for the privilege. Concepts like strike prices and expiration dates matter considerably here; dedicated options guides cover these in depth.

Swaps

A swap is an agreement to exchange cash flows or other financial instruments over time. Interest rate swaps are the most common: one party might trade fixed interest rate payments for floating rate payments with another.

Institutions typically use swaps to manage interest rate exposure, currency risk, or other financial variables. Unlike exchange-traded instruments, swaps are usually customized agreements negotiated directly between the parties.

Forwards

A forward contract resembles a futures contract: both involve agreeing today on a price for a transaction that settles later. The difference: forwards are private agreements between two parties, not standardized exchange-traded contracts.

Customization is the draw. Forwards can be tailored precisely to what the parties need. The trade-off is counterparty risk (the possibility that one side fails to meet their obligations).

Where Are Derivatives Traded?

Derivatives trade in two main venues, each with distinct characteristics and risk profiles.

Exchange-Traded Derivatives

Exchange-traded derivatives change hands on regulated exchanges like the Chicago Mercantile Exchange (CME) or Intercontinental Exchange (ICE). Contracts are standardized; all terms except price are set by the exchange.

Exchange trading offers several advantages:

- Transparent pricing visible to all participants

- Lower counterparty risk because the exchange stands between buyer and seller

- Greater liquidity, making it easier to enter and exit positions

- Regulatory oversight

Futures and many options trade on exchanges, making them accessible to institutional and retail traders alike.

Over-the-Counter (OTC) Derivatives

Over-the-counter derivatives are negotiated directly between two parties, bypassing exchanges entirely. Swaps and forwards typically fall into this category. OTC markets allow customized terms: valuable when standard contracts don’t fit specific needs.

The trade-off is higher counterparty risk. No exchange guarantees the transaction, so each party must evaluate the other’s creditworthiness and ability to perform. OTC markets are dominated by large financial institutions, corporations, and sophisticated investors.

Who Uses Derivatives?

Market participants range widely, each with different goals.

Institutional Investors

Pension funds, mutual funds, hedge funds, and insurance companies use derivatives extensively to hedge portfolio risk, gain efficient exposure to asset classes, or execute complex strategies. Institutional scale makes these players dominant in most derivatives markets.

Retail Traders

Individual traders can access certain derivatives, particularly exchange-traded futures and options. Participation has grown as trading platforms have become more accessible. Still, retail traders represent a smaller share of overall volume compared to institutions.

Corporations

Non-financial companies turn to derivatives primarily for hedging operational risks. A multinational might use currency derivatives to manage exchange rate exposure. An energy company might hedge against oil or natural gas price swings. For these businesses, derivatives function as risk management tools rather than speculative instruments.

Risks of Derivatives Trading

Derivatives serve legitimate purposes, but they carry meaningful risks that anyone considering them should understand clearly.

Leverage risk: Many derivatives let traders control large positions with comparatively little capital. Gains can multiply, but so can losses. In some cases, traders can lose more than their initial outlay.

Complexity: Derivatives can be difficult to fully understand, particularly the more sophisticated varieties. Misjudging how a contract behaves under different conditions leads to unwelcome surprises.

Counterparty risk: In OTC markets especially, there’s a real chance the other party defaults. Exchange-traded markets reduce this risk but don’t eliminate it entirely.

Market risk: Like any financial instrument, derivatives move with markets, and prices can shift rapidly, particularly during turbulent periods.

Liquidity risk: Exiting some derivatives can prove difficult, especially customized OTC contracts or thinly traded instruments.

Derivatives are powerful, but they demand genuine understanding of both the instruments and the markets they inhabit. They aren’t suitable for everyone. Anyone considering them should honestly assess their knowledge, experience, and tolerance for risk beforehand.

Key Takeaways

- A derivative is a financial contract whose value depends on an underlying asset—stocks, commodities, currencies, or interest rates

- The four main types are futures, options, swaps, and forwards, each with distinct mechanics and applications

- Derivatives serve three core functions: hedging risk, speculation, and price discovery

- Exchange-traded derivatives offer standardization and reduced counterparty risk; OTC derivatives offer customization but carry additional exposure

- Users include institutional investors, retail traders, and corporations managing business risks

- Significant risks accompany derivatives trading, including leverage, complexity, and counterparty exposure

Disclaimer: This content is educational and does not constitute financial advice. Derivatives trading carries substantial risk of loss and is not appropriate for all investors. Consider your financial situation and risk tolerance carefully before trading derivatives.

About the authors

Related articles

10 Economic Indicators Every Forex Trader Should Track

Learn which 10 economic indicators move forex markets, why each one matters, and how to use an economic calendar to trade smarter.

Forex vs Crypto: Which Market Has Better Risk-Adjusted Opportunities for Retail Traders?

Compare forex vs crypto on volatility, liquidity, regulation, and cost to find which market offers better risk-adjusted opportunities for you.

10 Forex Broker Red Flags to Watch Before Choosing a Forex Broker

Learn the 10 forex broker red flags that signal fraud or malpractice. Includes a step-by-step verification checklist and regulatory database links.

0 comments