Hedging Strategies in Trading: How to Protect Positions

Hedging offers traders a structured way to manage risk: offsetting potential losses in one position with gains in another.

In volatile markets, knowing how to hedge can be the difference between preserving capital and taking unnecessary hits. This guide covers the logic behind hedging, walks through the most common strategies, and helps you decide whether hedging belongs in your trading approach.

What Is Hedging in Trading

Hedging Defined

Hedging is a risk management technique where you open a secondary position designed to reduce or limit potential losses from an existing one. Think of it as insurance: you accept a smaller, known cost to protect against a larger, uncertain loss.

In practice, this means opening a position that moves opposite to your primary trade. If your main position loses value, your hedge gains value, compensating for part or all of that loss. The aim is to reduce your overall exposure when prices move against you.

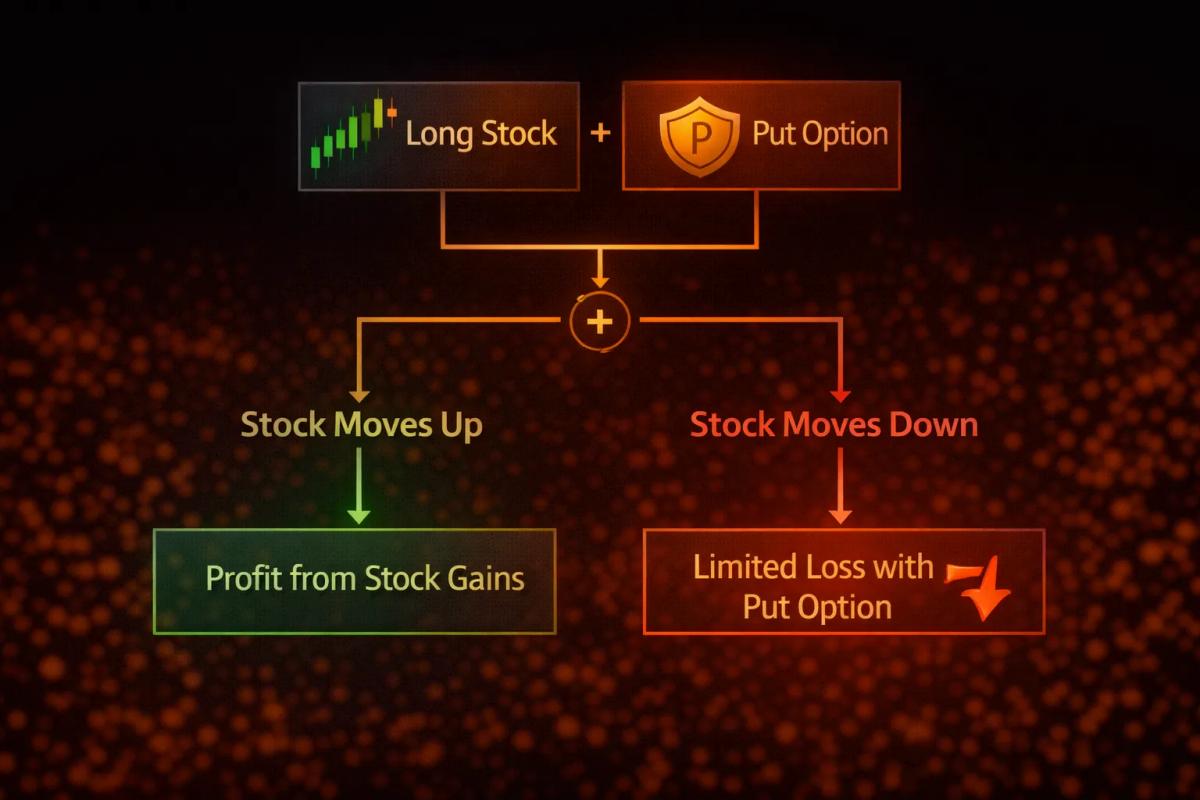

Say a trader holds shares in a company and buys a put option on that same stock. If the share price drops, the put increases in value, offsetting some of the loss. The put’s cost represents the premium paid for that protection.

How Hedging Differs from Speculation

Hedging and speculation sit at opposite ends of the risk spectrum. Speculation means taking on risk to pursue profit. Hedging means reducing risk by accepting a defined, limited cost.

A speculator enters a trade expecting to profit from price movement in one direction. A hedger already holds a position and wants to protect its value regardless of where the market goes. The speculator needs to be right about direction; the hedger needs only to limit damage when direction turns unfavorable.

This distinction shapes how traders measure success. A well-executed hedge might lower overall returns during favorable conditions, as protection costs eat into profits. But that same hedge prevents severe losses when conditions turn.

Why Traders Use Hedging

Managing Downside Risk

The core reason to hedge is downside protection. Markets can move against a position fast, and without a hedge, you absorb the full impact. Hedging lets you define your maximum potential loss upfront rather than leaving it open-ended.

Picture a trader with a large long position in a currency pair before a major economic release. The announcement could push prices sharply in either direction. Without a hedge, downside risk is essentially unlimited. With one (a protective option, an offsetting position) the trader caps the worst-case loss while staying exposed to potential upside.

Downside protection matters most when:

- Market conditions are uncertain or volatile

- A position has accumulated meaningful unrealized gains worth protecting

- External events create unpredictable risk: earnings, economic data, geopolitical developments

- You can’t actively monitor positions during high-risk windows

Preserving Capital During Uncertainty

Beyond individual trades, hedging serves a larger purpose: keeping your capital intact. Trading capital is finite. Large losses shrink the funds available for future trades and erode the psychological willingness to take necessary risks later.

Many traders treat hedging as a capital allocation decision. The cost of a hedge gets weighed against the potential cost of an unhedged loss, including how drawdowns compound over time to drag on long-term portfolio growth.

During periods of heightened uncertainty (ahead of central bank decisions, during market dislocations) hedging lets traders maintain positions without bearing unlimited risk. This can be preferable to closing out entirely, which might trigger taxes, rack up transaction costs, or miss a favorable move.

Common Hedging Strategies Explained

Direct Hedging (Opposite Positions)

Direct hedging means opening a position that exactly offsets an existing one.

A trader long 100 shares might short 100 shares of the same stock; a forex trader long EUR/USD might simultaneously go short EUR/USD.

This approach neutralizes market exposure. If price rises, the long gains and the short loses by the same amount. If the price falls, the reverse happens. Net exposure to price movement: zero.

Direct hedging is straightforward but has real limitations. Many brokers restrict or prohibit holding opposite positions in the same instrument. Holding two offsetting positions also ties up margin without creating any directional profit potential. Direct hedging works best as a temporary measure during extreme uncertainty, or when you want to pause a position without actually closing it.

Options-Based Hedging

Options offer flexible hedging because their payoffs are asymmetric. The most common approach is the protective put: a trader holding stock buys a put option on that same stock.

Here’s how it works:

- You hold shares and want protection against a price decline

- You buy a put option with a strike price at or below the current stock price

- If the stock drops below the strike, the put gains value, offsetting some or all of the stock’s loss

- If the stock rises, you benefit from the appreciation minus the cost of the put premium

Covered calls take a different angle. Here, a trader holding stock sells call options against those shares. This generates premium income that cushions modest downside, though it caps upside if the stock rises past the strike price.

Options-based hedging requires understanding how options are priced, how expiration affects value, and how strike price selection determines protection levels. Option costs fluctuate with market volatility, time remaining, and distance between strike and current price.

Pairs Trading as a Hedge

Pairs trading involves simultaneous long and short positions in two correlated assets. The strategy profits from relative performance (how one asset does versus the other) rather than from market direction.

A trader might go long one oil company while shorting another. If the oil sector falls broadly, the long position loses but the short position gains, partially offsetting the damage. Profit comes if the long outperforms the short, regardless of whether oil prices rise or fall overall.

Pairs trading hedges broad sector or market risk while isolating individual asset performance. It demands careful analysis of correlation patterns; the hedge only holds if the two assets actually move together in response to market-wide factors.

Diversification as Passive Hedging

Diversification functions as a form of passive hedging: reducing portfolio risk without requiring active management of hedging positions. Holding assets that react differently to market conditions naturally offsets losses in one area with stability or gains elsewhere.

A portfolio spanning stocks, bonds, commodities, and cash provides built-in hedging. When equities decline, bonds or gold may hold value or appreciate, softening the overall impact.

Unlike active strategies, diversification doesn’t eliminate risk on any single position. It reduces how closely portfolio returns track any one market factor. Diversification works better over longer horizons and may not protect against short-term swings in individual holdings.

When to Hedge and When Not To

Situations Where Hedging Makes Sense

Hedging delivers the most value under specific conditions:

- High conviction, high uncertainty: You believe in a position’s long-term thesis but face near-term event risk

- Concentrated positions: One holding represents an outsized share of portfolio value

- Illiquidity constraints: Exiting a position quickly isn’t practical when risk spikes

- Defined risk events: Known catalysts: earnings, elections, policy announcements create temporary volatility

- Protecting gains: Unrealized profits are large enough to be worth insuring

Hedging also makes sense when protection costs are reasonable relative to the risk.

If a protective put costs 2% of position value and guards against potential losses of 20% or more, the hedge may offer favorable risk-adjusted value.

Costs and Trade-Offs of Hedging

Hedging isn’t free. Every hedge carries costs that must be weighed against the protection:

Hedging may not be worth it when:

- The hedge costs more than reasonable loss expectations

- The position is small relative to overall portfolio

- Market conditions are stable with low volatility

- You can easily exit if needed

- Time horizon is short and risk tolerance is high

Hedging shouldn’t be reflexive. Each hedge represents a trade-off, and the math doesn’t always favor protection.

Practical Considerations Before Hedging

Choosing the Right Instrument

A hedge’s effectiveness hinges on instrument selection. The right hedging instrument:

- Correlates reliably with the position being hedged

- Offers sufficient liquidity to enter and exit cleanly

- Matches the time horizon of the risk

- Costs less than the expected value of the protection

Common choices include options, futures, inverse ETFs, and correlated assets in opposite directions. Each behaves differently:

- Options: Flexible with a defined maximum cost, but premiums can be steep when volatility is elevated

- Futures: Direct price exposure without premium decay, but require margin and may carry basis risk

- Inverse ETFs: Trade like stocks, but daily rebalancing creates tracking error over time

- Correlated assets: No direct cost, though correlation can break down precisely when you need it most

Sizing and Timing a Hedge

Sizing a hedge means deciding how much protection to buy relative to your position. A full hedge covers 100% of position value; a partial hedge covers less.

What influences hedge size:

- Cost tolerance: Larger hedges cost more

- Risk tolerance: Higher tolerance may justify smaller hedges

- Conviction level: Lower conviction suggests more protection

- Position importance: Core holdings may warrant fuller coverage

Timing matters because hedge costs shift with market conditions. Volatility drives options prices, so buying protection after volatility spikes gets expensive. Ideally, you establish hedges when protection is cheap, before uncertainty builds.

That said, waiting for perfect conditions can leave you unprotected when risk arrives without warning. Many traders hedge as routine practice rather than trying to time it precisely.

Key Takeaways

Hedging strategies serve a specific purpose: reducing exposure to adverse price moves while keeping you in the market. Knowing when and how to hedge, and when the costs outweigh the benefits, helps you make clearer decisions about managing risk.

Key points:

- Hedging reduces risk but doesn’t eliminate it; every hedge has costs and limitations

- Different strategies suit different situations: direct hedges, options, pairs trades, and diversification each have distinct profiles

- The decision to hedge should reflect specific circumstances, not a one-size-fits-all rule

- Effective hedging means matching instrument, size, and timing to the risk at hand

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Trading involves risk, and hedging strategies may not suit all traders or market conditions. Consider consulting a qualified financial professional before implementing any trading strategy.

About the authors

Related articles

Cognitive Bias in Trading: How Mental Blind Spots Hurt Your Results

Learn how cognitive biases like confirmation bias and loss aversion affect your trading decisions. Discover practical techniques to recognize and overcome them.

Common Trading Mistakes and How to Avoid Them

Learn the most common trading mistakes that cost beginners money. Discover how to identify and avoid these errors to protect your capital and improve results.

How to Create a Risk Management Strategy: A Step-by-Step Guide

Learn how to create a risk management strategy step by step. Build a risk plan with clear rules to protect your trading capital.

0 comments